Contact us today if you need individual or group Medicare coverage

Jessica Nuccio

(Toll Free) 1-833-236-3318 extension 4

Medicare Senior Advisor

401 E. Fairmount Ave.

Lakewood N.Y. 14750

Medicare is a government subsidized program designed to insure seniors and some younger disabled people (as determined by the Social Security Administration), as well as covering individuals with ALS and end stage renal disease. Medicare covers about half of the cost of medical claims for the covered individual, with the remaining costs being covered by other supplemental or separate insurance, or by paying out of pocket.

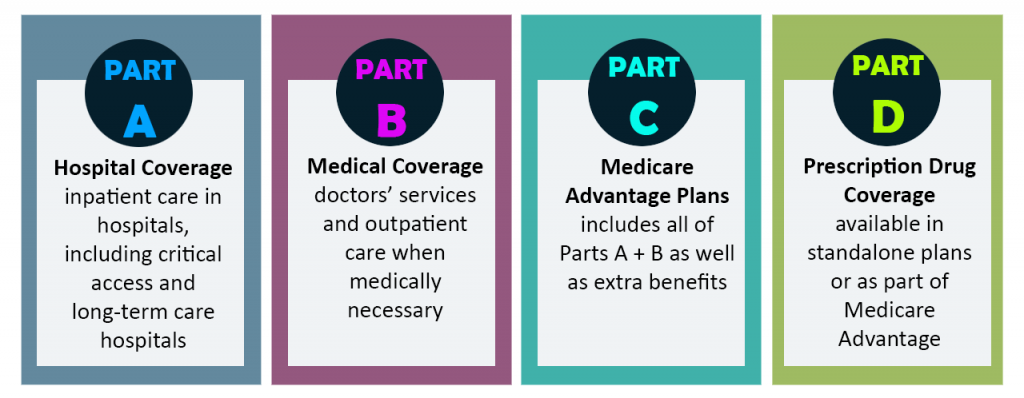

Medicare is broken down into several “Parts”, most commonly known as Medicare Parts A-D:

Part A is Hospital Insurance. Part B is Medical Insurance. Medicare Part D covers many prescription drugs, though some are covered by Part B. In general, the distinction is based on whether or not the drugs are self-administered. Part C health plans, the most popular of which are branded Medicare Advantage, are another way for Original Medicare (Part A and B) beneficiaries to receive their Part A, B and D benefits (basically Part C is a public supplement option that can be compared with group private supplemental Medicare coverage from a former employer or individually purchased private so-called Medigap insurance). All Medicare benefits are subject to medical necessity.

Medicare affects not only individuals approaching retirement age, but also employers who employ Medicare eligible individuals, their spouses, and employer sponsored retirement plans. Here we will go over how Medicare affects both the individual and the employer and the potential pitfalls of each.

For Individuals

Eligibility:

“In general, all persons 65 years of age or older who have been legal residents of the United States for at least 5 years are eligible for Medicare. People with disabilities under 65 may also be eligible if they receive Social Security Disability Insurance (SSDI) benefits. Specific medical conditions may also help people become eligible to enroll in Medicare.

People qualify for Medicare coverage, and Medicare Part A premiums are entirely waived, if the following circumstances apply:

- They are 65 years or older and US citizens or have been permanent legal residents for 5 continuous years, and they or their spouse (or qualifying ex-spouse) has paid Medicare taxes for at least 10 years.

- They are under 65, disabled, and have been receiving either Social Security SSDI benefits or Railroad Retirement Board disability benefits; they must receive one of these benefits for at least 24 months from date of entitlement (eligibility for first disability payment) before becoming eligible to enroll in Medicare.

- They get continuing dialysis for end stage renal disease or need a kidney transplant.

Some beneficiaries are dual-eligible. This means they qualify for both Medicare and Medicaid. In some states for those making below a certain income, Medicaid will pay the beneficiaries’ Part B premium for them (most beneficiaries have worked long enough and have no Part A premium), as well as some of their out of pocket medical and hospital expenses.” ¹

Source: wikipedia.org

Enrollment Periods

Enrollment periods for Part A&B are pretty straightforward for most of us, but how those dates interact with supplemental coverage can be confusing. Let’s cover some quick facts to answer those unanswered questions.

• In general you can enroll in Part A&B during your Initial Enrollment period which is the 7 months surrounding your 65th birthday. You can enroll in Part C Medicare Advantage and Part D Prescription drug coverage during your Initial Enrollment period which is the 7 months surrounding your 65th birthday, the Annual Election Period Oct 15 – Dec 7, and then disenroll during the Special Disenrollment Period Jan 1st – Feb 14.

• If you are turning 65 and you are in your initial coverage election period you can sign up for an Advantage Plan (with or without drug coverage) or a Medicare Prescription Drug Plan during your initial coverage election period. If you are getting Part B for the first time you can sign up for an Advantage Plan (with or without drug coverage) or a Medicare Prescription Drug Plan during your initial coverage election period. , but must due so between Between April 1–June 30.

• If you are newly eligible due to a disability you can sign up for an Advantage Plan (with or without drug coverage) or a Medicare Prescription Drug Plan during your initial coverage election period. during your Initial Enrollment Period. If you already had Medicare due to disability, but now you turned 65, you can sign up for an Advantage Plan (with or without drug coverage) or a Medicare Prescription Drug Plan during your initial coverage election period and change plans. ²

Late Enrollment Penalties

• If you don’t enroll in part D during your Initial Coverage Election Period you have 63 days to enroll. If you miss the window you may forever pay more for your Part D Drug Coverage due to a “late enrollment penalty” unless have “other creditable prescription drug coverage”, or you get “Extra Help”.

• If you don’t get Part B during your initial enrollment period you can end up paying more for life for that too. However some COBRA, employer based plans, union plans, and more can affect this. Check with your employer and Medicare.gov for specifics. ²

Medicare Compliance for Employers

Due to the Medicare Modernization Act, employers who provide prescription drug coverage to Medicare-eligible individuals must complete the Online Disclosure Form to the U.S. Centers for Medicare & Medicaid Services (CMS) to report whether such coverage is creditable prescription drug coverage. Creditable coverage means that the coverage is expected to pay, on average, as much as the standard Medicare prescription drug coverage. This disclosure must be completed within 60 days from your group plans’ renewal date.

If you have any of the following individuals on your health plan:

- Medicare eligible active working individuals and their dependents (including a Medicare eligible individual when he or she joins the plan)

- Medicare eligible COBRA individuals and their dependents

- Medicare eligible disabled individuals covered under your employer’s prescription drug plan

- Any retirees and their dependents

then you are required to do two things:

- Disclose the creditable status of all prescription drug plans to those Medicare-eligible individuals and

- Disclose to CMS the status of all plans offered to those individuals and when the individuals will be apprised of their plan status.

If you have Medicare-eligible individuals or employees who’ve already turned 65 but are still on your group plan, you must disclose to those individuals once per calendar year which plans have a creditable prescription drug component and which plans do not. This notice must be given to Medicare-eligible employees and their dependents prior to Medicare open enrollment, which is October 15th each year. If you have such employees, attached to this email are model notice forms to give to those Medicare-eligible individuals. These model notices are customizable and can be filled out by the employer for the Medicare-eligible individual to retain to prove they had creditable Rx drug coverage so the employee doesn’t get penalized (1% of premium per month) if they do decide to take a Medicare Part D plan in the future.

Contact us today if you need individual or group Medicare coverage